Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.

– Milton Friedman

Corporate Debt

While treasury yields have move up recently, after a decade of quantitative easing by central banks, interest rates are still extremely low. Low rates have also pushed other financial asset prices higher. If the last recession was induced by high real estate prices and corresponding high mortgage bond prices, this recession will be driven by high equity valuations and low yield of corporate debt. Generic US Junk Bonds have a yield of 6%, up from a low of 5.2% in 2017 (The default rate in 2017 was 4.5%, up from 2.3% in 2016). These interest rate levels have allowed corporations that should have failed under normal conditions to remain in business. If a company is selling a product or service that consumers no longer want, or if another company has a technological advantage over, the company would typically wind down or pivot to survive. However, when rates are low and demand for yield by fixed income investors are high, a weak or failing company can simply issue debt with light covenants to raise operating capital. They can continue to sell their product or service at a reduced rate, even if it means that the company is not profitable since debt carries the business, not the product. Consumers will purchase an inferior product if the price is low enough.

A recent example is Toys R Us, a company that would have normally failed much earlier than it did. However, Toy R Us took advantage of strong demand for yield in the last seven years. Low interest rates pushed up the cost of retail properties and subsequently rent for brick and mortar retailers, while Amazon was able to offer the competitive products but without the the same overhead expenses. This technological efficiency allowed Amazon to reduce prices on goods such as toys. Toys R Us matched prices, but at the cost of positive EBITDA. Eventually, their debt was no longer sustainable, as the company was servicing their debt with more debt issuance. This scenario took almost a decade to play out due to low rates. More companies that have been living off of debt issuance will soon face the reaper.

2008 Again?

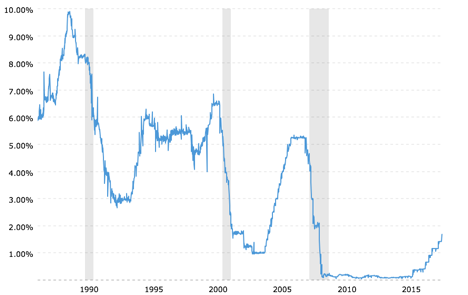

The last recession primarily hinged on easy credit for homebuyers. Homebuyers and speculators took advantage of low mortgage rates fueled by interest rates as well as innovative mortgage products that allowed homebuyers even lower rates, often variable rate spread to treasuries or Libor. Ten year US Treasuries, which is the benchmark for 30 year mortgage rates, went from 5.5% in 2002 to 3.25% a year later in 2003.

As the market began to heat up and asset prices rose (another way to say that inflation was setting in), the fed decided to raise rates to battle inflation. Higher interest rates led to the inability to purchase already unaffordable real assets at higher prices. Although the markets were very fragile, the Fed continued to raise rates until it was too late, eventually forcing the Fed and Treasury to work together to implement the largest purchase of assets to the Fed’s balance sheet in history, along with rates cuts. Central Banks around the world followed suit. Bank of Japan added assets equal to 96% its GDP, and even began to purchased ETFs when JGBs no longer produced a positive yield. ECB’s balance sheet is at 40% of GDP, while the Fed is at 23%.

The Next Recession

The Fed is single minded in its mandate of maintaining low stable inflation, which is 2% in modern times. Given the mandate and early signals of inflation coming, such as the recent spike in oil prices, we will likely see a Fed Funds rate of 2.5% by the end of the year, accomplished by three more rate hikes. This has two effects on corporate debt. First, most below investment grade debt is issued as bank loans and coupon is variable rate to LIBOR. This would mean at least a 1.5 points more in coupon interest paid by those companies on their debt going forward. This could be significant for a company that has $1B in variable bank loan debt. Second, companies that are facing maturity walls are now paying 1.5–2.5 points more interest when they refinance, if spreads don’t widen further by then. Spreads would widen if the current 4% default rate on corporate bonds increases to 9–10% by the second quarter of 2019, which would subsequently increase the average yield from 6% to 12%, wiping out the free cash flow of many below investment grade companies addicted to a low rate environment. Increases in risk-free rates, higher default rates, and higher spreads on corporates creates a vortex of defaults that spill into the equity markets and the general economy. The last two times the corporate default rate exceeded 10%, the S&P 500 lost over 40% of value. As Illustrated by the chart, rapid increases in rates have preceded the last three recessions.

Trade War Continues

Another factor is the current US/China trade war, which has the potential to drive inflation higher as cost of imports carry a tariff. Tariffs allow domestic producers of the same product to charge higher prices, pushing inflation higher. Higher inflation is the fuel that causes central bankers to increase interest rates.

Digital Assets

Increase in defaults and market downturns have a broad effect on all companies seeking to raise capital. I anticipate capital for the ICO market becoming more scarce, forcing out a lot of the bad deals. Additionally, technology sector companies, including businesses in the blockchain industry, will have a more difficult time securing funding by the end of 2018 and into 2019. This will create unique opportunities to find value in the Altcoin market. Additionally, Bitcoin and Ethereum prices, like Gold and precious metals, are generally a function of supply and demand. There is no data, only speculation, on how these assets will perform in a recession, but I included a Gold chart, beginning with Bretton Woods in 1944, Nixon’s Economic Stabilization Act of 1970, and the end of Bretton Woods in 1976. There is no correlation between gold and equities in the last 40 year relevant period. There has been a correlation between digital assets and certain equity markets, but only in the last two out of their ten years of existence. This is mostly due to Bitcoin appearing at the same time as the beginning of the latest economic cycle, as equity prices have moved higher, and digital assets have been independent. The lack of correlations should continue through the end of this economic cycle, however, as digital assets earn a place in broad portfolios and blockchains gain wider adoption, I believe higher correlations will begin to appear and they will be regarded as risk assets.

The Next Recession: Corporate Debt was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.