Part 1 — Ripple, XRP & International Payments.

Bitcoin, the largest of all crypto assets, seems to be stabilising in price. With a Market Capitalisation of a Trillion Dollars and ongoing investment flows from institutions, 1000% price increases over 12 months may be a thing of the past for BTC.

As Bitcoin goes mainstream, speculative money seems to be flowing away from largest cryptocurrency into ‘Altcoins’. These are assets with a lower a market cap, but at the same time greater latent potential for enormous asset appreciation.

The point of this series of posts is not to speculate on which of these ‘Altcoins’ is best placed too x10 or x1000 over the coming year. Some certainly will, and there is enough resources on the internet for that already.

The goal is to share how some of these ‘Altcoins’ are based on incredibly interesting projects, which I have a real chance to disrupt the retail industry moving forward.

After all, the reason for starting this blog is to explore wider blockchain technology and brainstorm its application to the retail industry as a whole.

In evaluating these each of these blockchain projects, I like to run little thought experiment. I ask myself;

How could this disrupt Retail today?

Which of these offer an improvement to the current way of doing things?

Which am I most interested in?

From my own explorations and self education, many of these ‘Altcoins’ have little underlying value or application. Many seem to simply exist as a vehicle for speculation.

Nevertheless, there are a few projects that I am excited about, with a real potential to disrupt my own business moving forward.

The first of these is Ripple; which promises a future of fast and frictionless International payments.

That right there is an exciting idea.

My company, is an international distribution business based on the importation and sale of premium consumer brands from the around the world. We specialise in finding beauty brands with strong domestic market, but a desire to expand their reach into new countries.

We are based in London, and thus are an attractive second market for most of the brands we talk to. We have formed partnerships with companies in Switzerland, the USA, Russia, India and Italy. For each of our partners we make cross border payments to import their goods into the UK Market and sell them on through our domestic network.

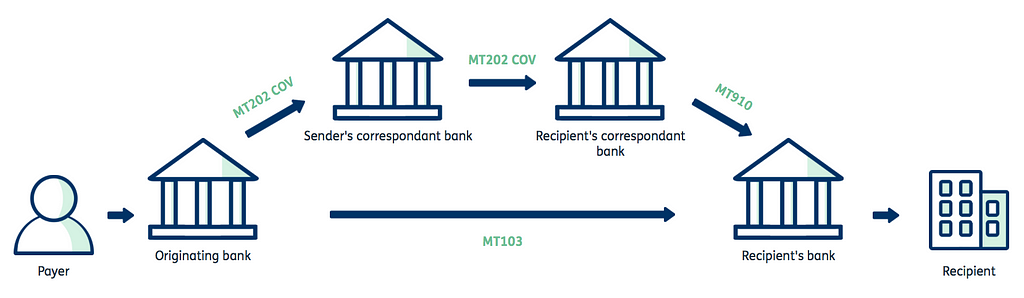

Today, cross border payments through a bank are still cumbersome and slow. Currently, we use SWIFT payment services. SWIFT is a messaging network that banks and other financial institutions use to securely transmit instructions through a standardised code. Currently there is about 11,000 financial institutions within the SWIFT network, and it has been Go-to technology for international payments since its inception in 1973.

For us, a payment to our supplier in New Orleans, in the USA in can take 1–4 days to process with SWIFT. But to the city of Pune, in India, payments can take up to 2 weeks to be received.

In India, financial institutions there are unlikely to be within the same direct SWIFT network as our bank in the UK. Consequentially, our payment needs to be routed through a number of different banks before it can reach the bank accounts of our supplier there.

For every international payment with SWIFT we make, we have to a pay a transaction fee based on the number of banks our payments funds are channeled through. Further, we also need to blindly accept the exchange rate the bank offers us, with no transparency on how the rate is calculated. On top of all of that, every SWIFT payment made is accompanied by a 5% failure rate, usually related to administrative and data input reasons.

Although the SWIFT messaging service has been the Gold standard in international payments since its inception in 1973, it is often, slow, expensive and sometimes unreliable.

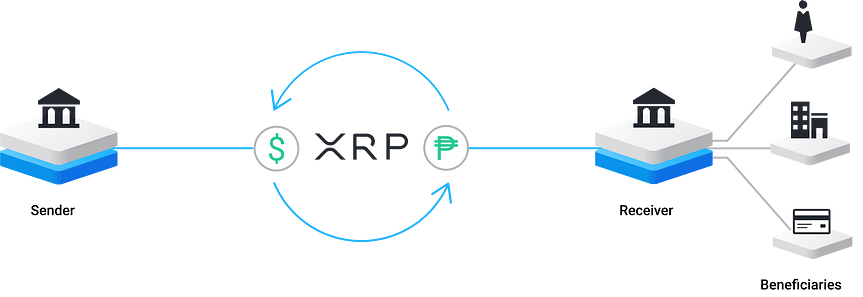

Ripple is a blockchain based project that enables immediate international payments. It does this by providing on demand liquidity for cross border transactions in the form of its well known Cryptocurrency — XRP.

Unlike SWIFT, the payment funds from our bank account do not need to move through a number of different banks, before being received by our suppliers.

Ripple’s utilises XRP, its underlying crypto asset, as a bridging currency between the paying bank and the recipient bank abroad. As such, the time lag and the expensive fees are eliminated.

If transactions using Ripple were widespread and adopted by our domestic banks, the process of making international payments would be instantaneous, cheap and reliable. We could pay a sole trader in India with the same efficiency by which we could pay a large corporation in the USA.

The World Bank itself said:

“De-Centralised Ledger Technology based cross-border payments potentially offer a promising pathway to dramatic improvements in the lives of millions of people in emerging economies. DLT could improve the traceability of remittances and reduce compliance costs for MTOs and supply chain payments, stimulating economic activity in destination countries.”

Its. my deduction that the only thing in Ripple’s way is the Network Effects that SWIFT already has in place, given that is has been connected to almost every major bank in the world through 200 countries for over 30 years.

If it can overcome that hurdle, Ripple seems to be a project with a long race to run.

Even if Ripple itself doesn’t win out, a blockchain based solution to international payments seems to be far superior to any currently utilised technology.

The ‘Altcoin’ Disruption of Retail was originally published in DataDrivenInvestor on Medium, where people are continuing the conversation by highlighting and responding to this story.