Summary:

- Securitization of small businesses (on blockchains and other distributed ledgers) and fractionalization of real assets are gaining momentum. It’s only good for business punks right now, but soon it’ll take a legitimate form. It seems that in the life of capital markets, we’re at a spilled-milk moment: the climate is changing, not the weather. Things will never be as they used to be. Once set loose, the mutation won’t stop because financial tokens have a wide avenue open to proceed to dynamically programmable investor relations, and from there they can create a completely new big data layer that will feed yet another AI monster.

- The transition from legacy to blockchain-recorded (tokenized) assets has started and even if it halts and dies somewhere on the way, the limited period when the world will be temporarily overloaded with junk security tokens (and broader, financial tokens) is imminent anyway because it’s right next on the adoption curve. The most serious organizational challenge will be in dealing with the stratification of various types of issuers and “pseudo-underwriters”. It’ll take a lot of altruism from business people to self-coordinate themselves. Some serious suffering is unavoidable.

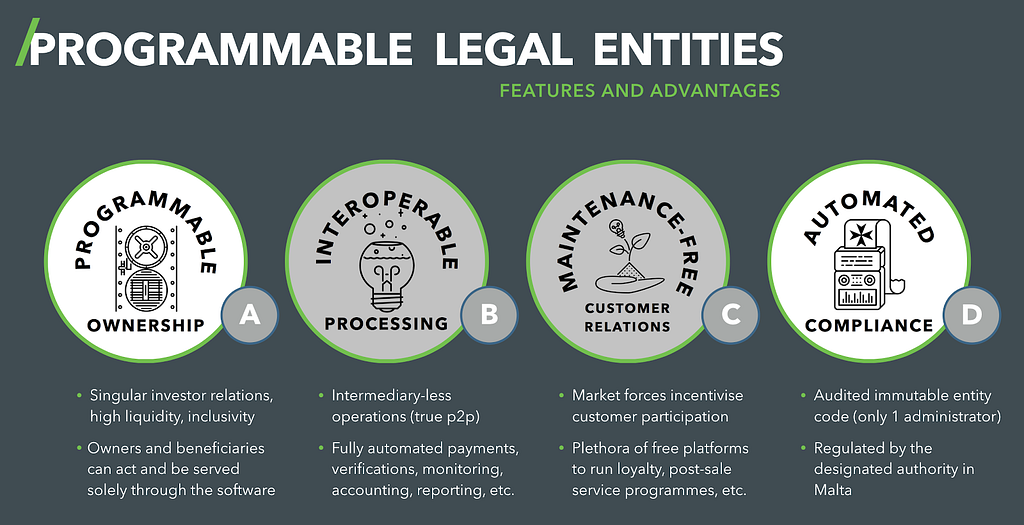

- However, the above described things are not really important when compared to the main outcome: the birth and broad adoption of programmable legal entities. The gambling of crypto and the real, objective need for easier securitization and fractionalization played the role of the Trojan horse, introducing much more important innovation.

From Securities to Financial Tokens

Many fruits of progress started with a backward-looking appearance. First cars were not cars, they were horseless carriages. It wasn’t harmless. Dangerous weight distribution on the chassis with no aerodynamic design, neglect of free incidental electricity on board, and other mistakes that would be obvious for a heritage-free mind have severely devalued the modernization. A short while later, of course, the features of carriages and phaetons have all but vanished, but the first years the only innovation in power was the dismissal of the horse.

In the case of investments, the horse is His Majesty the Accountant. Today, accounting systems dominate the processes of issuance and circulation of securities. The terms between the entrepreneur and the investor are mostly defined by an instrument standard (for example, a share of a stock that gives the right to receive dividends and vote) and the rules the particular exchange has to obey.

Financial tokens take away the function from a whole layer of intermediaries who have successfully institutionalized themselves in the wet gap between the entrepreneur and the investor over the past centuries.

Need to pay dividends? The token will do. Need to ensure the right to vote? No problem. Any function of any existing investment instrument can be coded in a few lines. Even more astonishing from the traditional perspective: the very same token can be traded on any number of exchanges.

The stage of mimicry with the traditional form is inevitably followed by a deep and pragmatic exploitation of the entire technological potential. It will soon be admitted that the extreme standardization of securities is a historically justified but clearly outdated compulsory measure.

Uninstalling mediators in investments is only the beginning. At the next step, well-established investment scenarios, such as stocks and bonds, may give way to sophisticated, customized, almost “complete contracts”.

From Financial Tokens to Dynamically Programmable Investor Relations

Some technologies are so existentially important that Nature insistently pushes their introduction, by hook or by crook, on board of some Trojan horses. For example, rockets are necessary for the survival of mankind as we can’t inhabit a spare celestial body without them. The technology was already well understood in the nineteenth century, but it took the senseless quarrel between maniac dictators many decades later to actually pay for it, with the money that was robbed from the crippled peoples.

The programmability of legal entities was always needed. At the very least, to reduce tax fraud. Software finally finds its way into every facet of our lives; it is quite strange that it took so long to penetrate into a sphere of that significance. Finally, in 2018, gambling has played the role of the Trojan horse in introduction of this technology.

The sin of compulsive gambling is as old as time and absolutely ineradicable. The business of extracting money from addicts has mutated many times. Only in the last twenty years we have seen the rise of filthy “forex”, binary “options”, online “casinos”, and most recently — ICOs of “utility tokens”.

In a typical good country, gambling is mainly regulated to channel the evil, not to replenish the treasury. In the same vein, building sport arenas and maintaining fan cults is the cheapest way to neutralize the inevitable few percent of aggressive population. However, for a few dwarf countries, selling offshore gambling licenses is simply a cynical export of vice.

But there is also a gray intermediate zone, when the authorities see both short-term profits and incentives for long-term development. For example, it has always seemed controversial how tolerant Israeli authorities are to the fact that their land wielded the world’s largest technological hub for the organization of trading in extremely dubious forms, despite the fact that it is strictly prohibited to sell such “products” to the citizens of the country. But it was clever of them. Malta did something even smarter this year.

It is difficult to say to what extent Maltese legislators succumbed to the lobbying efforts of the global “ICO and crypto-trading elite”, and to what extent they became interested in the prospects of regulated financial tokens. It is important that the bureaucrats found good experts and formed a very logical layer of legislation. They could have simply legalized the circulation of cryptocurrencies and tokens, but they doubled-down and created a special governing body to work with new business entities (this is a huge breakthrough, for in most countries they are trying to push it to one of the existing dominions) and introduced a new, special type of legal (programmable) entity.

The latter circumstance will not manifest itself for some time. Companies will issue tokens, exchanges will gain licenses, people will invest and speculate. Token markets will be perceived as complementary to traditional ones. However, the hook on which the institution of investments hangs today has already been broken.

Perfect Storm

I see three factors that will integrally give the transformation process an enormous power:

- Practically infinite growth potential for securitization and fractionalization.

- Strong independent incentives on both ends of the classic two-sided market.

- A powerful civilizational perspective.

Practically Infinite Growth Potential

In physical estimations, there is a professional practice to simply neglect the values two orders of magnitude down from the characteristic one for the considered process. That is, if your billiards balls are 200 grams each, specks of two grams on the table is something you ignore.

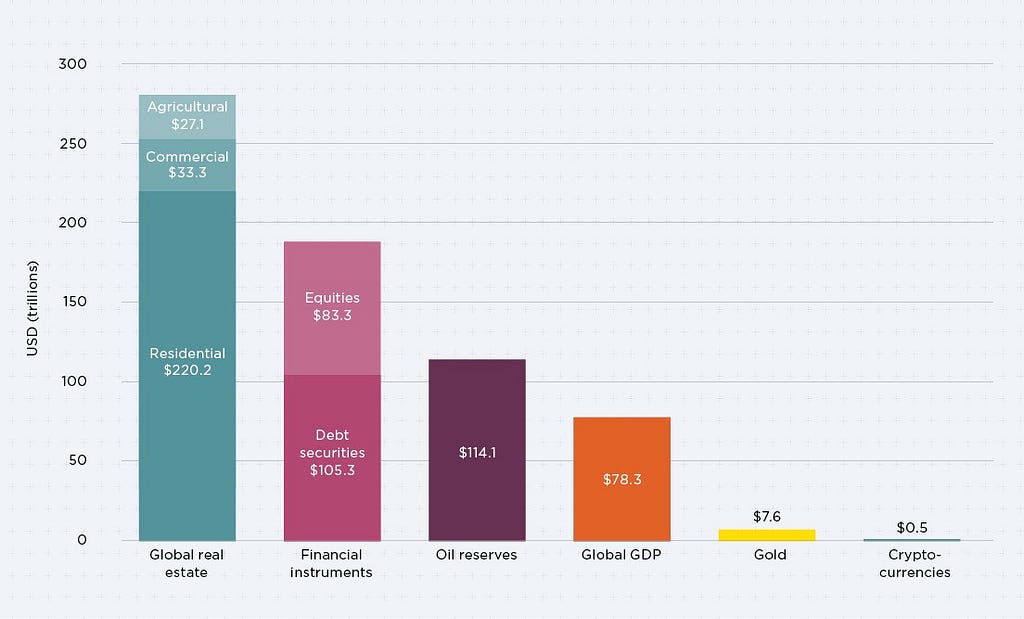

What share, do you think, of the world’s wealth is already put into circulation today? In other words, how much worth can be freely bought and sold, more or less, in relation to everything that is of monetary value on this planet (we’re talking real stuff — abstract derivatives do not count)?

Surprisingly, no more than 1%! To begin with, the largest asset class, real estate, is practically not securitized. There are, of course, a variety of funds in which you can buy shares but, in practice, it is impossible to “short Palo Alto” or “long Brooklyn”, for a reasonable amount of money.

We can safely expect that in the presence of a convenient technological framework, a few percent of these three-hundred trillion dollars will be securitized in no time at all. In addition, in several years the market of agricultural land should face the tectonic shifts due to the introduction of cultured meat. So, securitization comes in very handy.

But securitization of small business will create the most powerful wave. The aggregate value of small business is much higher than the market capitalization of public companies. In the current situation, it is extremely difficult and expensive to bring small enterprise stocks to an exchange, while almost all owners want it. Titanic amounts of money will enter.

Strong Independent Incentives

One fair objection may be that most people won’t rush to buy the shares of small businesses, as a company is small probably because it is simply not good enough to grow. True, but do not forget about the factor of programmable entities. Many new “small tokens” can be born as a result of an artificial fragmentation of a bigger traditional enterprise. Programmable legal entities will allow the creation of modular management and libraries of “standard firms”. The complexity of the software structure can be increased indefinitely, as opposed to manually managed organizations.

If you have shares of a large company, you are forced to sponsor all its initiatives, including, for example, flirting with the military, expensive attempts not to look like a monopolist, and dozens of dead projects. The company cannot issue shares on a project basis, but tokens issued by an interconnected group of programmable legal entities is quite a realistic approach.

It is important to abstract from the old patterns and recognize that individual, contractual relations is what investors should reasonably want and demand. And companies need it too. Economically responsible opinions of thousands of people is worth a lot. This may be a whole new facet of crowdsourcing.

New Class of Big Data

Elon Musk recently expressed the thought that people on this planet were put into the role of the limbic system under the cortex of global social applications. As in the case of an individual, the cortex is “smarter”, but it is in the servant position to the limbic system which is the generator of happiness.

With the broad adoption of programmable legal entities, it will be the turn of businesses, as independent “smart” units, to directly become “slaves” of new big data accumulators. I think we will soon see completely new forms of the network effect.

The aggregate expectation is clear: even if the existing capital market is a powerful pickup truck, at least several dump trucks are flying across its way.

Potential Difficulties

All tokens are authentic, and their security level is generally considered equal to the transport blockchain’s. However, each family of tokens will be backed up by a different unconditional legal promise of the issuer, varying in quality, just like fiat currencies (there are reserve ones, there are ordinary ones, and there are junk ones). A token, being a negotiable instrument, can be legally enforced to be redeemed by the party in possession but with a different effort.

The above creates a stratification problem when various underwriters will create and use tokens representing same class nominal property and value but different redemption reality. Of course, the market price will reflect that but the high speed and convenience of digital exchanges do not takes us any closer to the high standards of the legacy environment. There will be just too many issuers. Jurisdiction that will follow Malta (and they will follow) will need time to make their rules interoperable, even if they have the will.

To reduce stratification and to avoid the future assets space from devolving into a junkyard, competing agencies will offer paths to operator validation procedures. That might do the opposite and increase the chaos of the transition period. It’s going to be filtering war against the creeping invasion of shit-operators in an environment of good operators being stubbornly conservative.

Maybe the altruistic evolutionary mechanisms will be turned on. This is probably the case where the format/standard war is not good for anyone. Should we see one stratum showing some traction, others should join their standard rather than compete.

Pony up, Folks! Programmable Legal Entities are Tectonically Reshaping Capital Markets was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.