Introduce yourself to the FINTECH World and beyond!

Complexities turning into Opportunities

What is the first thing that comes to most of the people’s mind when they think of Financial services!

A complex world !!!

To some extent, it is true as the financial services like lending, depositing, payments, insurance happen in coordination with banks, government regulations and compliance/mandates which is not so easy to get familiar with. In today’s digital world where we can access entertainment or can connect with anyone instantly, Finance access is yet to come to this state where this is accessible by almost anyone in the world.

Take for example a typical credit card payment you make today, as a consumer or merchant we do not realise the complexity it has to go through in processing a transaction. There are authorisations, address verifications, batch submittals, captures, chargebacks, clearings, currency conversions, holdbacks, interchange fees, and settlements happens in the background and there are multiple players involved in doing this like acquirers, issuers, payment facilitators, and processors. There are also card associations, such as Mastercard, Visa, American Express, and Discover.

Now the question that might come to your mind “why would I really have to worry what happens in the backend”

Well, these are complexities for some but an opportunity for FINTECH players to explore and create solutions which in turn help consumers, Merchants, Banking institutions!

Now let’s try to understand what complexities some of the Fintech players are dealing with.

A look at some of the Fintech players and FinServices area

- Stripe noticed the Regulatory complexity, a byzantine global financial system, and a shortage of engineers are constraining the impact of the internet economy. In addition, whether you’re looking to bill customers on a recurring basis, set up a marketplace, or simply accept payments, do it all with a fully integrated, global platform that can support online and in-person payments.

- Robinhood noticed the complexities involved around investing in Stocks, ETFs and Options especially for millennials (aged from 18 years to 29 years) and created solutions in the form of an app to make these look easier.

- Klarna one of Europe’s largest banks and is providing payment solutions for 60 million consumers across 130,000 merchants in 14 countries. Klarna offers direct payments, pay after delivery options and installment plans in a smooth one-click purchase experience that lets consumers pay when and how they prefer to.

- Although Oscar can’t dismantle and rebuild the broken health care system on our own, we can work every day to offer you more for your money, give you access to the best doctors, and make your experience within the health care system better. Oscar has stated that its aim is to change Americans’ experience of engaging with the healthcare system by “redesign[ing] insurance to be geared toward the user experience.”

- Kabbage is a technology company that quickly connects small businesses with capital. Their technology platform reviews data generated by dozens of business operations to automatically understand business performance and deliver fast, flexible funding entirely online.

So how to go about understanding the fintech world, let’s start with the understanding of Money and Banking which is the foundation of Fintech industry.

Concept of Money and Bank!

In the primitive age, Barter was the medium of direct exchange where goods and services are exchanged for other goods and services. To some extent, it can be a good approach in case the mutual negotiation between 2 parties go well. The problem arises when the value of the exchange is questioned!!

That is when the concept of money comes up. Money helps in determining the value of the goods which in turn will be used in the transaction.

An issue with the barter system can be the storage of goods. In contrast to barter, money is generally less costly to store although there are storage costs here too.

When entrepreneurs found this issue of value and storage they started trusting “Banks” which would tell them to keep their money safe with them and in turn they will give you interest.

Now when people started saving their money in banks, banks also started to lend a portion of that to other projects which can create more opportunities and in turn, wealth can be created.

A bank is a financial institution that accepts deposits from the public and creates credit. Lending activities can be performed either directly or indirectly through capital markets. Due to their importance in the financial stability of a country, banks are highly regulated in most countries. Most nations have institutionalised a system known as fractional reserve banking under which banks hold liquid assets equal to only a portion of their current liabilities. https://en.wikipedia.org/wiki/Bank

There are several old banks(Like Barclays which was Established in year November 17, 1690) and still operational and running! But what innovation Banks brought to the consumers and entrepreneurs!!

The most important financial innovation that I have seen the past 20 years is the automatic teller machine, that really helps people and prevents visits to the bank and it is a real convenience. How many other innovations can you tell me of that have been as important to the individual as the automatic teller machine, which is more of a mechanical innovation than a financial one?[https://nypost.com/2009/12/13/the-only-thing-useful-banks-have-invented-in-20-years-is-the-atm/]

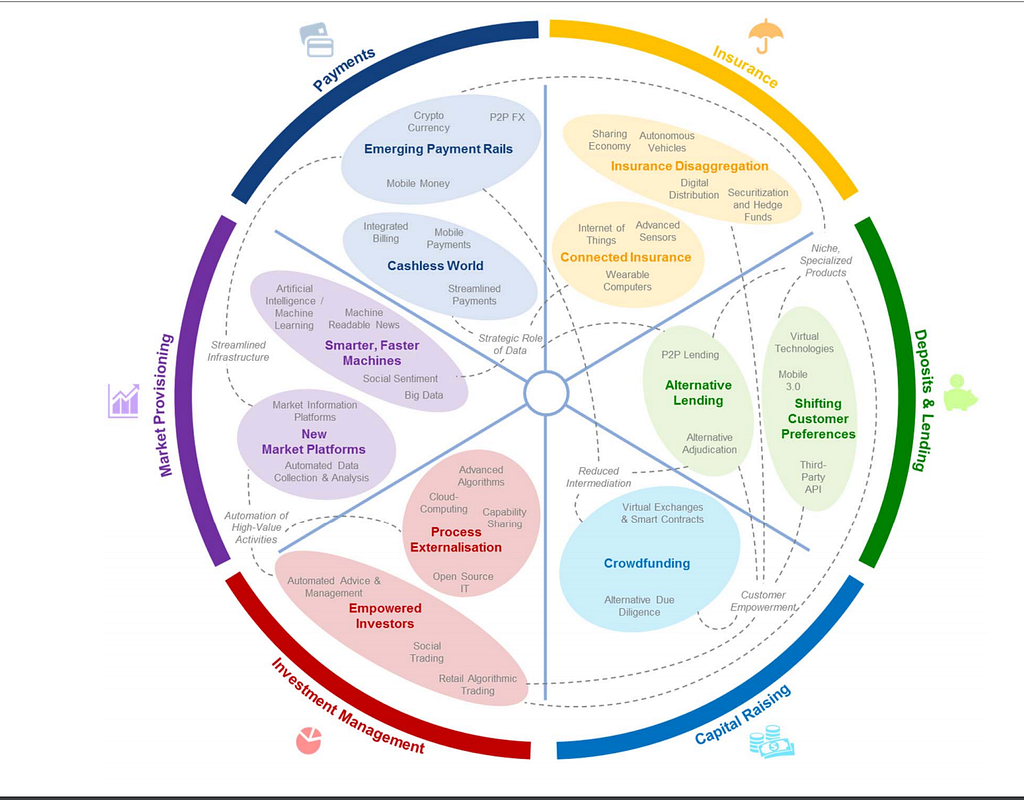

Financial Services Framework

World Economic Forum in its research structured the financial services into six major functions as shown below.

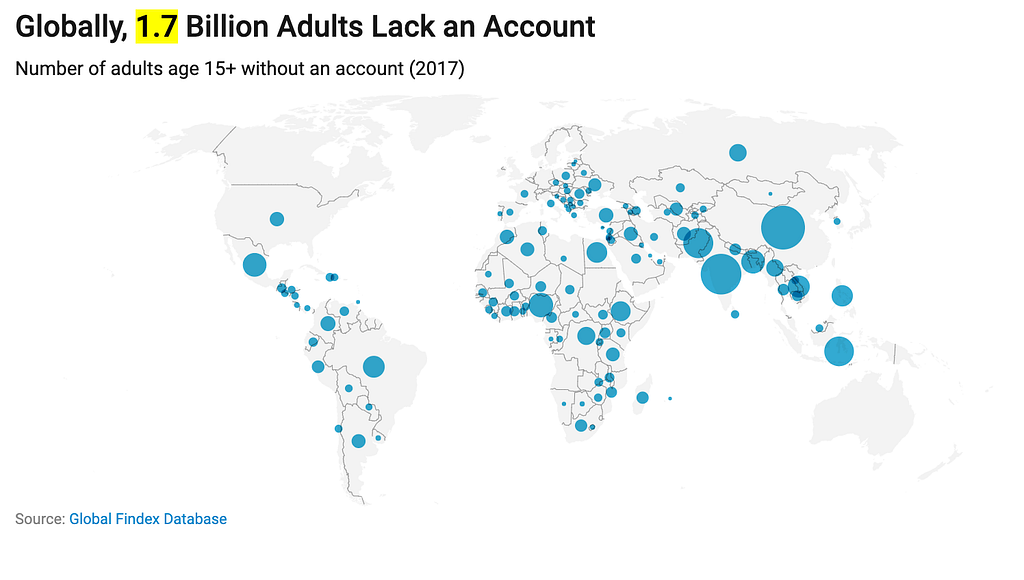

The question is how to enable everyone in the world with financial information?

As per World Bank report, Globally, 1.7 billion adults remain unbanked, yet two-thirds of them own a mobile phone that could help them access financial services. Fintech can indeed help and enable these people get access to financial services with the help of technology.

World Bank Group President Jim Yong Kim said. “Financial inclusion allows people to save for family needs, borrow to support a business, or build a cushion against an emergency. Having access to financial services is a critical step towards reducing both poverty and inequality, and new data on mobile phone ownership and internet access show unprecedented opportunities to use technology to achieve universal financial inclusion.”

Let’s fast forward and get into the age of technology and internet which is changing the game!!

Internet, Mobile Technology and Data— the Game changer!!

In the information age, when people are connected and exchanging information quickly. When we can send messages across the world with a single click then why can’t the financial services like payments are achieved the same way!!

Banks had to keep pace with this fast advancement of technology. They still have legacy systems and connecting them require efforts.

Today, we have publicly available APIs and open source technology. We have modern hardware and open source databases. Small merchants can use mobile phones as POS [point-of-sale] terminals, enabling them to accept credit cards instead of just cash or checks. — Jason Gardner, founder and CEO of Marqeta

With the power of technology and growth in financial services, FINTECH questions the wisdom of traditional financial sectors by providing consumers and business with more features, more choice and more access to financial services than ever before!

BlockChain technology and Bitcoin

The story on Fintech cannot be completed without touching on BlockChain technology which is revolutionising the entire financial services key framework areas and innovating it further.

BlockChain technology also called distributed ledger technology is a database where information is recorded in multiple instances and anyone in the network can access and verify or add to it. There is no centralised authority instead, protocols help manage the network.

One of the implementations of this technology is Bitcoin. In the physical world paper cash can be transferred between two people without the involvement of banks then why can’t we achieve the same in the digital world. Bitcoin a digital token (also called cryptocurrency) does this in the digital world to do the settlement then and there without the involvement of an intermediary.

BlockChain technology is bringing new possibilities in the world of Finance.

“There are 3 eras of currency: Commodity based, politically based, and now, math based.” — Chris Dixon, Co-founder of Hunch now owned by eBay, Co-founder of SiteAdvisor now owned by McAfee

So what next!

Fintech is all about how the financial services are provisioned, structured and consumed by leveraging the innovating technology! In the years to come, we will see how this is explored further.

Although fintech is only one piece of the global financial services ecosystem, it is rapidly evolving into something on the scope and scale of social media and online search.At minimum, it will fundamentally alter the way we relate to the numerous financial systems that support and surround our daily lives. -Mike Barlow

Money->Banking->Financial Services->Technology =>FinTech was originally published in Data Driven Investor on Medium, where people are continuing the conversation by highlighting and responding to this story.