Decentralization disrupting the finance ecosystem

Most comprehensive guide to the decentralized finance ecosystem

It has become a trend for almost every crypto start-up proponent to tout their business fundamentals leveraging the decentralization values of blockchain technology.

(Disclaimer: The content in this article is not sponsored by anyone and the views mentioned in this are solely of the writers. First seen on Nuo)

But, is every crypto project based on a decentralization principle?

In this article, we’ll decipher how Decentralised-Finance protocol based businesses are different from the traditional ones:

We’ll be mainly covering two main aspects

1) What’s De-Fi in its true sense?

2) What are the kinds of De-Fi platforms and their major differences?

The Ultimate Guide to De-Fi Protocols

Users of the traditional financial system often wish for a system that is more accessible and transparent, charges low transaction fees, and is less reliant on intermediaries. For such a fairer financial system to emerge, banking, lending, and derivatives have to undergo a radical transformation. Also, the adoption of a decentralized ecosystem such as DeFi needs to happen. It facilitates peer-to-peer borrowing and lending, eliminating centralized control, and providing financial freedom to the users.

Lately, in the crypto realm, there is much talk about decentralized finance, or DeFi for short. It offers global access to financial services: loans, derivatives, and other products; and has reduced or no role for conventional financial intermediaries. Proponents of the decentralized financial systems are seeing DeFi, also called open finance, as a great alternative to traditional lending. Some are already calling it the future of lending and borrowing.

DeFi is built on public blockchains such as Bitcoin network and Ethereum. It has become one of the “core drivers of usage” on the Ethereum network. By leveraging the permissionless, distributed networks, DeFi platforms transform the financial products into trustless protocols, which can be accessed by anyone from any part of the world. People who have no accounts in banks can also use DeFi solutions for lending and borrowing assets, as well as for trading with financial instruments.

The open-source platforms offer their users great benefits, including transparency, cheap cross-border transactions, no credit checks, and reduced censorship. Anyone can execute financial activities as there is no geographical location restriction.

How Decentralized is DeFi?

In recent months, there has been a surge in the introduction of DeFi solutions. All of them do not offer similar features and advantages. They have different models, and their degree of decentralization varies as well. Some DeFi models are less decentralized compared to others. It is because only a couple of their components have been decentralized, while the rest are still centrally controlled by the company.

Development of protocol, non-custody, price feeds, determining the interest rate, provision of margin call liquidity, and initiation of margin calls are the key components of a DeFi protocol. They determine the degree of effective decentralization.

A DeFi protocol is more decentralized than other models if the number of decentralized components is greater. Such a protocol would give users complete control over their digital assets, getting rid of centralized controls. Until now, no DeFi protocol has decentralized all the components. Each DeFi protocol is assigned a category that is based on the number of decentralized components.

Centralized Finance (CeFi): DeFi solutions are typically non-custodial, which means the users have control over their funds and are responsible for their security. CeFi, on the other hand, is custodial. A centralized system has the custody of the users’ assets, and it is also responsible for ensuring the security of their funds.

Users have no control over any aspect of the funds when it comes to lending or borrowing them. Interest rates are determined centrally, as well as the liquidity for margin calls is offered by a central system or authority. CeFi products use centralized price feeds, and initiation of margin calls is not permissionless. Celsius and SALT are considered CeFi solutions.

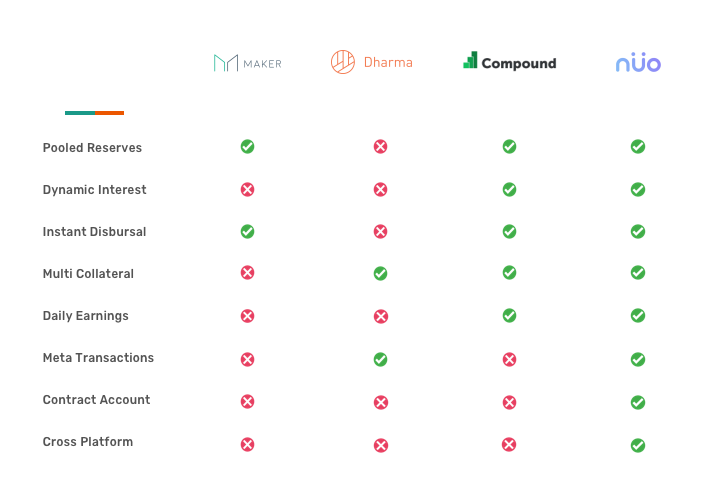

Degree 1-DeFi: This category DeFi product is non-custodial, and that is all it has to offer on the decentralization front. Its other components are very much centralized, just like the CeFi solution. Users cannot determine the interest rate, manage the development or updates of the platform, or offer liquidity for margin calls. The product uses decentralized price feed; centrally initiate margin calls. Dharma is one of the best examples of degree 1 DeFi. It is a peer-to-peer marketplace on Ethereum.

Degree 2-DeFi: The DeFi solutions in this category are non-custodial, and offer minimal financial freedom to their users as only one more component is decentralized. The decentralized component can be platform development or updates; price feeds, initiation of margin calls, provision of margin call liquidity, or interest rate determination. Except for non-custodial and one more component, the rest of the degree 2 DeFi protocol’s components remain centrally controlled. Nuo Network is an example of degree 2 DeFi.

Degree 3-DeFi: This category DeFi solutions feature two decentralized components, along with the non-custodial factor. Compound and MakerDao are examples of degree 3 DeFi protocols. They have permissionless initiation of margin calls as well as permissionless provision of margin call liquidity. Users have no control over interest rates or development of platform; both are centrally controlled in this category DeFi protocols. Price feeds are managed centrally as well.

Degree 4-DeFi: In products under this DeFi category, interest rates and development of platforms and updates are controlled centrally. However, unlike the degree 3 DeFi solutions, price feeds are out of central control. Protocols such as Fulcrum and dYdX use decentralized price feeds. Also, they feature non-custodial component, and permissionless initiation of marginal calls and provision of margin call liquidity.

Degree 5-DeFi: The degree 5 DeFi products offer users almost complete control over their digital assets. Only the platform development component is centrally managed. Example of degree 5 DeFi protocol is bZx, the first decentralized margin lending protocol on the Ethereum mainnet. This category product is non-custodial, with decentralized price feeds. Participants determine interest rates. Also, the initiation of margin calls and the provision of margin call liquidity are permissionless.

DeFi Platforms Advantages against Centralized Platforms and Centralized Banking System

- Users of centralized platforms can’t transfer borrowed funds to other trading venues and platforms. DeFi platforms offer this benefit to users. They are free to borrow capital and transfer it to multiple venues.

- Unlike centralized platforms, DeFi platforms offer users full custody of digital assets. If they want to enter margin trading, which is buying and selling of securities in a single session, they can do so. Users can keep the tokens as well as short an asset on a decentralized network.

They cannot do so if they are using centralized platforms, where the funds are managed centrally, and not everyone can take part in margin trading due to restrictions and jurisdictions.

- DeFi platforms eliminate the need for KYC.

- Unlike a centralized banking system, the interest rates on DeFi’s P2P lending/borrowing platforms are determined by market forces and not regulators.

- The information about the loans can be easily accessed by the participants and that too at no cost or a nominal cost.

- The DeFi platforms are more transparent and efficient than traditional banking platforms.

- Users can easily borrow funds at market rates, and the transaction process is very fast, as there are no intermediaries involved to facilitate the lending process.

- Not everyone can access banking systems, but everyone who has an internet connection can access DeFi platforms.

How to Use a DeFi Platform?

Crypto Lending/Borrowing is one of the hottest trends in cryptocurrency innovation right now, with many companies jumping on the bandwagon while figuring out the novel ways to make a place for themselves in this unconventional infrastructure of financial lending products by integrating blockchain technology.

Let’s take a deep dive to analyze the industry leaders in this domain!

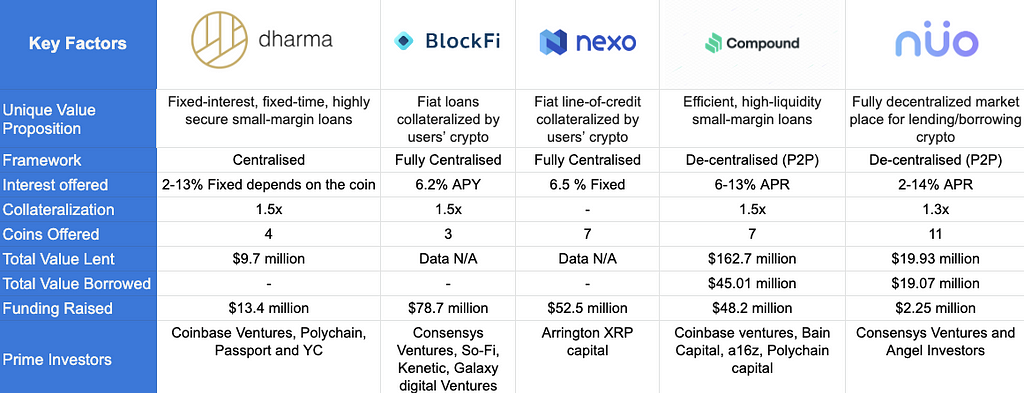

Compound vs Nuo vs Dharma vs Nexo vs Maker

Key considerations to analyze these platforms are the viability of the product, market fit, rates/collateralization, degree of decentralization, liquidity, funding & traction, and biggest value proposition.

Out of the above 5, only Compound and Nuo are the two fully decentralized platforms.

Compound Protocol: It establishes money markets, which are pools of assets with algorithmically derived interest rates that are based on supply and demand for the assets. It allows users to earn interest or borrow Ethereum assets without involving counterparty. However, unlike the Nuo Network, the Compound protocol does not allow direct lending. The assets supplied by the owners become part of a fungible resource from which other users can borrow funds.

Check out Compound!

New users will have to use community-built interfaces to access Compound protocols and markets, including the Compound Interface, Zerion, InstaDapp, and more.

- Lenders: Lenders supply assets to a market, and these assets are represented by ERC-20 token balance. Nuo Network enables lenders to earn interest every day, while Compound protocol’s interest rate fluctuates in real-time based on supply and demand. The interest rates are low when there is ample liquidity, and when the demand exceeds supply, the interest rate increases. Lenders are free to withdraw anytime.

- Borrowers: Users can borrow from the protocol using cTokens as collateral, and the borrowed asset gets directly transferred to their wallets. The market forces determine the borrowing cost for each asset. Users cannot borrow unless they have enough collateral in their accounts.

Nuo Network: It is a debt marketplace that offers a non-custodial way to lend, borrow, or margin trade digital assets. Nuo protocol allows users to create debt reserve, enabling them to earn interest on their digital assets every day. Users can easily borrow ETH or ERC20 tokens from debt reserves by staking collateral in the network’s smart contract.

Check out Nuo

Both long and short term loans are available, and users can borrow them at the interest rate that they prefer. The transactions are delegated to the contract, and post-order matching, they are executed. There is a password-encrypted private key for signing transactions. And all the transactions can be verified on-chain.

New users need to create a Nuo account with Metamask/Web3 Wallet or password-based signup. They will have to transfer ETH or ERC20 tokens to this account, and after that, they can start lending or borrowing on the platform.

- Borrowers: Once they have added ETH or ERC20 token to their Nuo smart account, borrowers need to create an over-collateralized loan or place a margin trade with up to 3X leverage. The system matches the loan to an ETH or ERC20 reserve, and after that, the funds are transferred in the Nuo account very quickly. Borrowers will need 1.5x of the loan amount as collateral to get the loan.

- Lenders: They create debt reserve, which is lent to borrowers based on their loan request. The interest that lenders earn depends on the number of loans funded by the reserve. The interests are accrued in a reserve contract and distributed proportionally and periodically every day. Once the debt reserve is canceled, the total amount plus the accumulated interests would get transferred to the lenders’ trading account.

Conclusion

DeFi is still in its nascent stages, but advocates of the decentralized financial systems have already declared that it has enormous potential. It is currently the most “active sectors” in the crypto realm, and its growing popularity cannot be dismissed as a fad. A recent market report stated that the DeFi protocols have grown “spectacularly” in less than a year. The value locked in DeFi had increased to more than $500 million from $181 million in a year.

The report also predicted that by the end of 2020, the total value locked might surpass $1.5 billion. If DeFi protocols gain widespread acceptance, they will most likely reshape the financial instruments, decentralize lending and borrowing, and make financial systems less fragile, and more transparent and more resilient.

Compound vs Nuo vs Dharma vs Maker | Which one is the best? was originally published in Data Driven Investor on Medium, where people are continuing the conversation by highlighting and responding to this story.