History of blockchain

To start, let’s talk about the history of the blockchain. Before it was ever used in cryptocurrency, it had humble beginnings as a concept in computer science — particularly, in the domains of cryptography and data structures.

The very primitive form of the blockchain was the hash tree, also known as a Merkle tree. This data structure was patented by Ralph Merkle in 1979, and functioned by verifying and handling data between computer systems. In a peer-to-peer network of computers, validating data was essential to make sure nothing was altered or changed during transfer. It also helped to ensure that false data was not sent. In essence, it is used to maintain and prove the integrity of data being shared.

In 1991, the Merkle tree was used to create a “secured chain of blocks” — a series of data records, each connected to the one before it. The newest record in this chain would contain the history of the entire chain. And thus, the blockchain was created.

In 2008, Satoshi Nakamato conceptualized the distributed blockchain. It would contain a secure history of data exchanges, utilize a peer-to-peer network to time stamp and verify each transaction, and could be managed autonomously without a central authority. This became the backbone of Bitcoin. And thus, the blockchain we know today was born, as well as the world of cryptocurrencies.

What is blockchain

The blockchain is an undeniably ingenious invention — the brainchild of a person or group of people known by the pseudonym, Satoshi Nakamoto. But since then, it has evolved into something more significant, and the main question every single person is asking is: What is Blockchain?

For investors new to the cryptocurrency world, one of the most overwhelming and confusing aspects can be blockchain. Blockchain technology is what powers and supports the digital currency space, and many analysts believe that it contains numerous viable applications and uses beyond cryptocurrencies as well.

By allowing digital information to be distributed but not copied, blockchain technology created the backbone of a new type of internet. Initially devised for the digital currency, Bitcoin, the tech community is now finding other potential uses for the technology.

The security is built into a blockchain system through the distributed timestamping server and a peer-to-peer network, and the result is a database that is managed autonomously in a decentralized way. This makes blockchains excellent for recording events — like medical records — transactions, identity management, and proving provenance. It is, necessarily, offering the potential of mass disintermediation of trade and transaction processing.

WHAT CAN BLOCKCHAIN TECHNOLOGY DO?

Make no mistake about it. The blockchain is a highly disruptive technology that promises to change the world as we know it. The technology is not only shifting the way we use the Internet, but it is also revolutionizing the global economy.

By enabling the digitization of assets, blockchain technology is driving a fundamental shift from the Internet of information, where we can instantly view, exchange and communicate information to the Internet of value, where we can immediately exchange assets. A new global economy of immediate value transfer is on its way, where big intermediaries no longer play a significant role — an economy where trust is established not by central intermediaries but through consensus and complex computer code.

Blockchains have the potential to change the nature of transactions, money and the global economy. The technology has applications that go way beyond apparent things like digital currencies and money transfers. From electronic voting, smart contracts & digitally recorded property assets to patient health records management and proof of ownership for digital content.

Blockchain will profoundly disrupt hundreds of industries that rely on intermediaries, including banking, finance, academia, real estate, insurance, legal, healthcare, and the public sector — amongst many others. This will result in job losses and the complete transformation of entire industries. But overall, the elimination of intermediaries brings mostly positive benefits. Banks & governments for example, often impede the free flow of business because of the time it takes to process transactions and regulatory requirements.

Blockchain technology will enable an increased amount of people and businesses to trade much more frequently and efficiently, significantly boosting local and international trade. Blockchain technology would also eliminate expensive intermediary fees that have become a burden on individuals and businesses, especially in the remittances space.

How does it work?

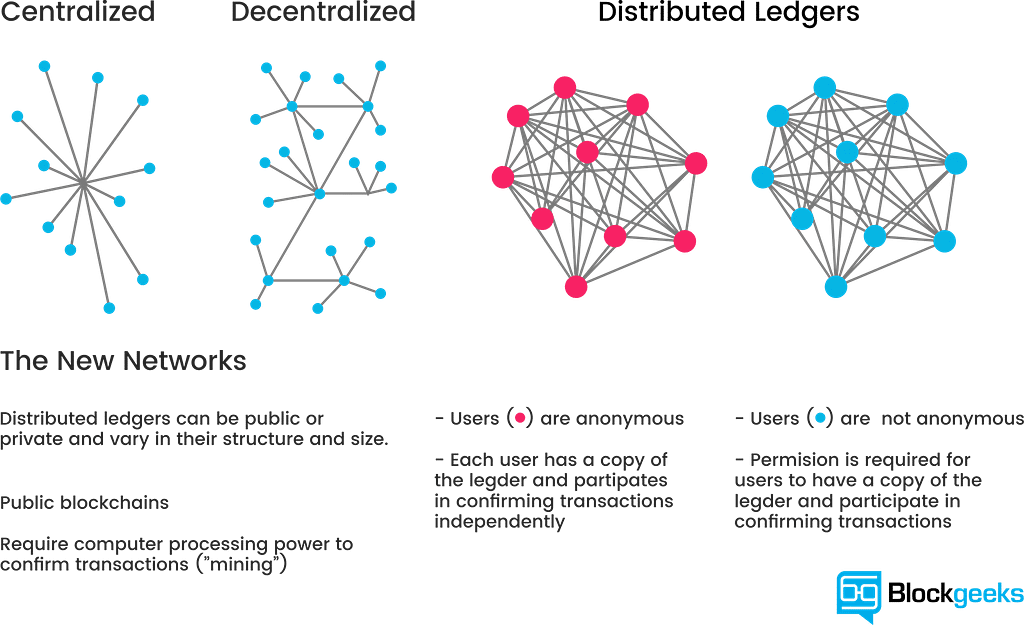

The bitcoin blockchain is “decentralized,” meaning it is not controlled by one central authority.

While traditional currencies are issued by central banks, Bitcoin has no central authority. Instead, the bitcoin blockchain is maintained by a network of people known as miners.

These “miners,” sometimes called “nodes” on the network, are people running purpose-built computers that are competing to solve complex mathematical problems to make a transaction go through.

For example, say lots of people are making bitcoin transactions. Each transaction originates from a wallet which has a “private key.” This is a digital signature and provides mathematical proof that the trade has come from the owner of the portfolio.

Now imagine lots of transactions are taking place across the world. These individual transactions are grouped into a block, organized by strict cryptographic rules. The block is sent out to the bitcoin network, which is made up of people running high-powered computers. These computers compete to validate the transactions by trying to solve complex mathematical puzzles.

The winner receives an award in bitcoin.

This validated block is then added onto previous blocks creating a chain of blocks called a blockchain.

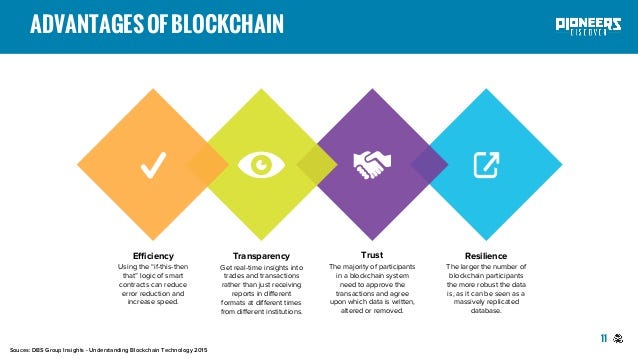

What are the benefits of blockchains?

The blockchain is attractive to some different constituencies for a variety of reasons, including the following:

The lack of a requirement for a central authority makes it an ideal ledger and settlement solution for joint ventures and affiliate relationships that are generally made on an equal or 50/50 footing without a provision for an arbitrator or manager. Indeed, having the computers verify transactions and settle them eliminates the need for clearinghouses and other settlement agents, providing disintermediation in a business arrangement and generally reducing costs while improving the speed at which transactions can be made, verified, settled, and recorded.

The digital signatures and verifications make it difficult to envision a scenario wherein a lousy actor could cause fraud and introduce problems that are costly to remove and resolve. The cryptographic integrity of the whole pending transaction, as well as examination by multiple nodes of the blockchain architecture, protect against threats and malicious use of the technology. (It is important to note that this security protection has mostly been untested in the marketplace and, while keen on a theoretical basis, questions remain about how well the protections will hold up in the reality of the digital economy we live in today.

The concept of blockchain works well at tracking how assets move through a supply chain, through certain vendors and factories to transmission and transportation lines and into their final locations.

References:

What is Blockchain Technology? A Guide For Beginners. (2018, July 16). Retrieved from https://nisanthvijay.wordpress.com/2018/07/16/what-is-blockchain-technology-a-guide-for-beginners/

Thompson, C. (2018, September 05). How Does the Blockchain Work? Pt. 1. Retrieved from https://www.sitepoint.com/how-does-the-blockchain-work-pt-1/

Reiff, N. (2018, June 15). How Does Blockchain Work? Retrieved from https://www.investopedia.com/tech/how-does-blockchain-work/

Lafaille, C., & Chantelle. (2018, September 27). What is Blockchain Technology? An Easy Guide For Beginners (2018). Retrieved from https://www.investinblockchain.com/what-is-blockchain-technology/

Hassell, J. (2016, April 14). What is blockchain and how does it work? Retrieved from https://www.cio.com/article/3055847/security/what-is-blockchain-and-how-does-it-work.html

Blockchain Oversimplified: A Beginners Guide To Blockchain. was originally published in Data Driven Investor on Medium, where people are continuing the conversation by highlighting and responding to this story.