This was adapted from one of my lectures at the Tekedia Mini-MBA program where I taught New Technologies, Growth, Disruption Innovation.

Introduction

Blockchain technology revolutionizes the way we store and share data by storing data in a Secure, Flexible, and auditable way. Harvard Business Review even said it has the “Potential to create new foundations for our economic and social systems.”

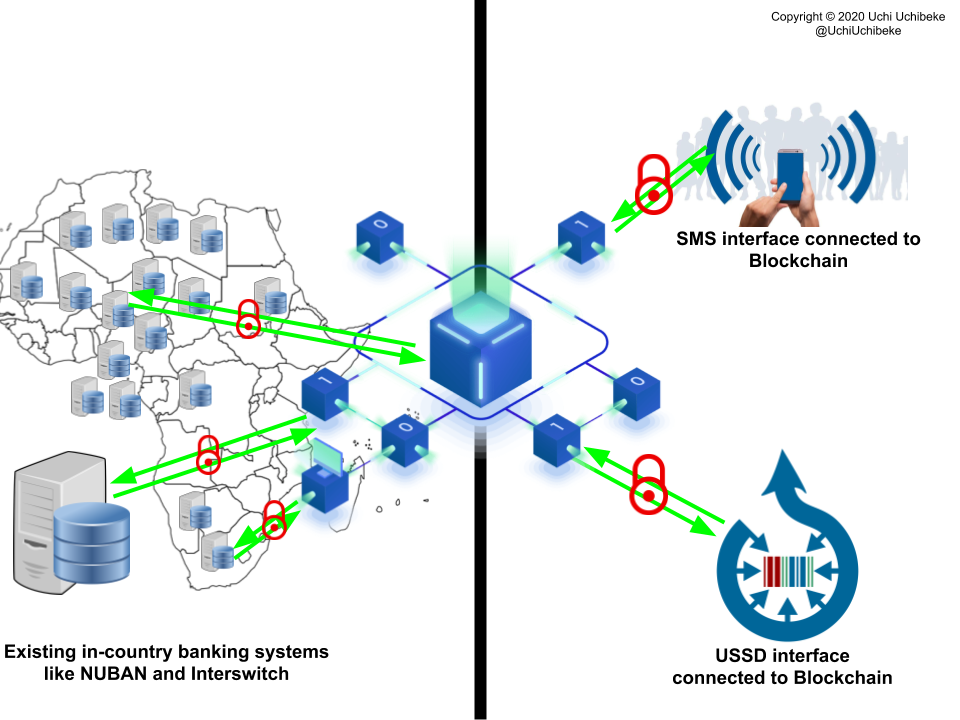

Blockchain is a network of computers that all agree on a unified ledger of information. The distributed ledger records transactions in a secure, flexible, verifiable, and permanent way. Transactions in a blockchain can be an exchange of an asset, the execution of the terms of a smart contract, or an update to a record. Blockchain technology is revolutionizing the way we store and share data and other digital artifacts. It, thus, has the Potential to digitally-enable businesses and opens new forms of revenue generation as it has done with Bitcoin and other cryptocurrencies.

Blockchain has the potential to create new foundations for our economic and social systems. — Harvard Business review

The benefits of Blockchain

The benefits of Blockchain does not only lie in cryptocurrencies but in the opportunities provided by Blockchain technology itself. Public blockchains like the bitcoin blockchain work well for cryptocurrencies. However, financial institutions, governments, and enterprises desire some control and privacy hence the shift towards private and permissioned or permissionless blockchains. Private blockchains, like Hyperledger Fabric, have seen wide adoption by financial institutions like the big banks in Canada and IBM because they provide the benefits of Blockchain in a private and permissioned manner. Four key benefits make Blockchain crucial for rapid transformation in the 4th industrial revolution (Industry 4.0):

- Tamper-proof: A thoroughly documented history of all data and changes are available in the chain

- No single point of failure: If a node fails, the rest of the network compensates

- Ransomware Resistant: Viruses like WannaCry would have to compromise every single node at the same instant to hold the data hostage

- Cryptographically secure: Uses industry best cryptography to make the data tamper-proof

Blockchain in the Wild

Onboarding customers 1000x faster at a Canadian Bank

Why? The problem

At a Bank, data was not being shared among different lines of Businesses in the same Bank due to technical or business reasons. It felt like customers were redoing their Drivers’ test every single time you wanted to buy a new car or rent one.

Imagin the Bank customer, Jenny, walks into the Bank to sign up for a product or service, let’s say a savings account with the Private/Personal Banking division of the Bank, she has to go through a rigorous background check; which consists of things such as reconfirming his identity, risk tolerance and so much more! All this information is then stored in the Bank’s private/personal banking database. Now, let’s say that Jenny wants to sign up for an investment account within the Securities division of the Bank. She would have to redo the entire signup process because sharing data between lines of Business is, unfortunately, is very challenging and the bank needs to by KYC and AML regulation complaint. This leaves Jenny buried in all the paperwork from the products and services she’s signed up for across the Bank. This creates a frustrating client experience for her. In this bank, the lengthy process that occurs when a client signs up for an account with another line of Business can take up to 2 weeks before the client is signed up.

Challenges

- There is duplicated work for employees as well as duplicated data across the Bank

- It’s costly to get to know our clients. It costs the average Bank 100 million dollars for this process.

- Lastly, the current process is not as secure as it should be!

How blockchain was used in the company

To solve the challenge, a team was put together to understand the problem. Because this was a process challenge and many back-office processes happen before a client is unboarded, the team studied the employees, traveled to bank branches to talk to managers and client services staff, and interviewed many executives before coming up with a Blockchain client identity management ecosystem called VERI. VERI is a scalable ecosystem that manages the digital client identity and product signup process across different lines of Business, using Blockchain Technology.

VERI offers many of the benefits of blockchains as outlined below:

Permissioned and Private: VERI was built using a permissioned and private blockchain, so only clients can start the signup process. That means only the departments that need to see the data can access it.

Flexible: Since it is flexible, it’s effortless to cater to the needs of different Lines of Business, and they can create custom workflows on the Blockchain.

Permanent: Blockchains allowed the Bank to keep a permanent record of data, and it’s a history of changes, which makes auditors happy and keeps the Bank at ease knowing data maintains its integrity. This creates one verifiable source of information.

And lastly, due to it’s distributed and decentralized nature, there’s no single point of failure and provides high availability

Components of the Solution

- A backend Blockchain which is where the magic happens,

- A mobile application used by existing clients of the Bank, which is baked right into the existing Bank app, and

- A Web App used by employees and approving authorities.

When a client wants to sign up for a product, they use their verified digital identity to fill out the application form automatically. Depending on the custom workflow specified by the line of business, the employees of the Bank can review and approve the submission so that the account can then be opened. This verification process satisfies the strict regulatory requirements. The method developed by the team is patent-pending both in the USA and Canada.

Benefits to the Company

The solution not only solves the Banks data sharing problem but also has additional benefits. Three of the foremost benefits include:

- It helps the Bank understand clients by giving them a holistic view of clients so they can provide personalized products and services

- It saves the Bank up to 33mm dollars annually

- And it reduces a two weeks process to 20 minutes, i.e., 1,000x faster

This all improves the client experience.

Future and Potential of the product

The team used two lines of Business as use cases for the new Blockchain solution. However, they designed Veri to be highly scalable so the Bank can plug in services from Credit card, Mortgage, and other departments at the Bank so clients can use their digital identities to sign up for services in these departments. They do this by providing an interface that allows the Bank’s employees to add custom workflows and forms without any technical skills.

5 Industry Transforming Blockchain Applications | Data Driven Investor

The solution has the Potential to power services for asset exchange, settlement, and cognitive analytics. The possibilities are endless, and in the future, a Bank with this solution can potentially allow smaller banks and companies to use their platform for user identity verification and make money in the process.

Buycoins Africa: Naira to Cryptocurrency Platform

Why? The problem

There was no easy way to buy Cryptocurrencies using your Nigerian Naira or bank account. People had to buy US dollars then use that US dollar to purchase the Cryptocurrencies.

Challenges

- There is duplicated work and for Nigerians who needed Cryptocurrencies because they had to spend time to transfer to US dollars and then to Cryptos.

- It’s costly to get to own Cryptocurrencies in Nigeria; in fact, it costs the average user 5% of the amount they are spending.

- It is very time-consuming.

How tech was used in the company

They provide a Blockchain platform that serves users’ needs of buying, selling, storing, or transferring Bitcoin, Ethereum, and Litecoin — as conveniently and quickly as possible.

To solve the challenge, the founders put together a team of Designer, Developers, and product people. Next, they built mobile apps that likely connect to a Blockchain network to store, process securely, and update user and transaction information.

Buycoins Africa reduces the time it takes to complete the purchase of Cryptos to 0.

Benefits the Company and Africa

The Buycoins platform provides a seamless way to buy/sell Cryptocurrencies across Africa hence enabling commerce between Nigeria and other countries without the need to exchange to US dollars first For the company, three areas that the benefits are:

- They make a profit from trade fees charged for peer-to-peer transactions and other fees and from data play. From their website, they mention that their margin on peer-to-peer trading transactions is very low. Although this is lower than any other platform on the continent like LocalBitcoins (1%), Remitano (1%), and Paxful (1%), Buycoins still makes some money.

- And it reduces the time it takes to complete the purchase of Cryptos to 0 because transactions are completed and settled instantly.

Future and Potential of the product

Transaction data and user transaction patterns could be valuable for future product roadmaps and inter-country transfers between African countries.

https://medium.com/media/0707f5c806284d01a4a13c7b13a91ce3/href

Blockchain: Digital Currency vs. Identity Currency was originally published in Data Driven Investor on Medium, where people are continuing the conversation by highlighting and responding to this story.